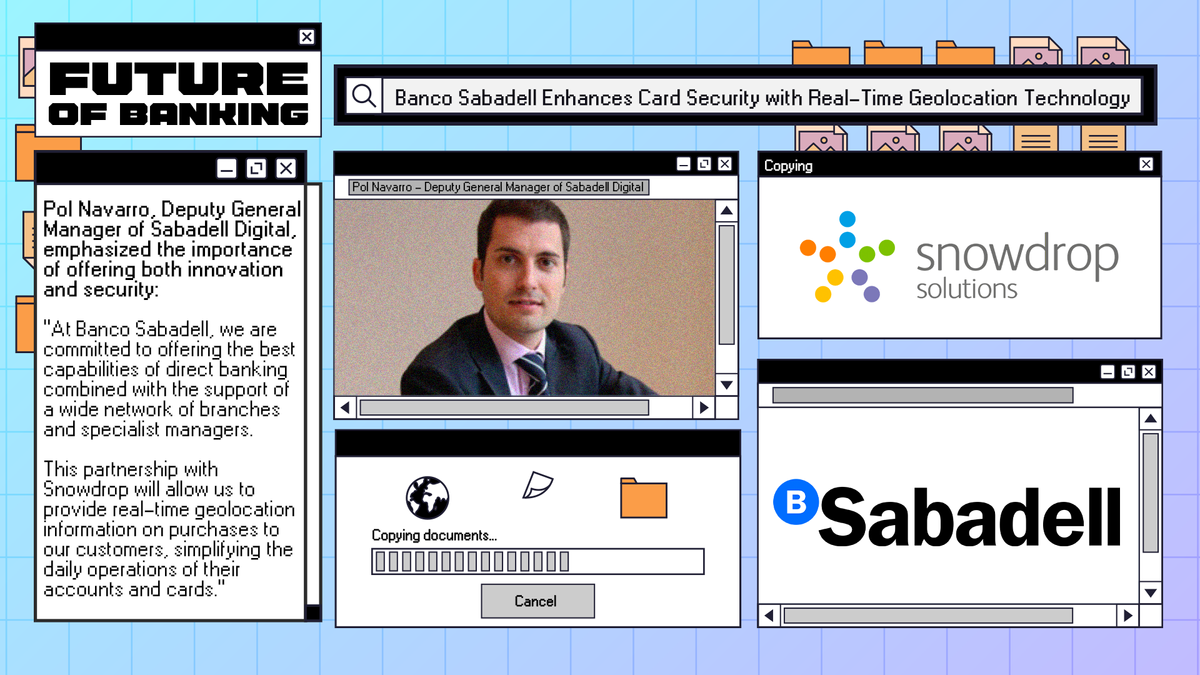

Banco Sabadell Enhances Card Security with Real-Time Geolocation Technology

Hey Digital Banking Fanatic!

Banco Sabadell has partnered with Snowdrop Solutions to launch transaction enrichment technology that displays card transaction locations on a map alongside merchant names and logos. The feature, powered by Google Maps geolocation services, enables customers to view their purchase locations in real-time.

Pol Navarro, Deputy General Manager of Sabadell Digital, stated: "At Banco Sabadell, we are committed to offering the best capabilities of direct banking combined with the support of a wide network of branches and specialist managers. This partnership with Snowdrop will allow us to provide real-time geolocation information on purchases to our customers, simplifying the daily operations of their accounts and cards."

The enhancement aims to improve transaction verification and fraud prevention by allowing customers to quickly identify suspicious activity through precise location tracking of their purchases.

If you’re interested in reading more about what’s been happening in Digital Banking, keep scrolling!

Cheers,

Subscribe to my Spanish Daily FinTech Newsletter for daily updates and analysis on the evolving world of financial technology—entirely in Spanish. Join now and stay in the loop!

INSIGHTS

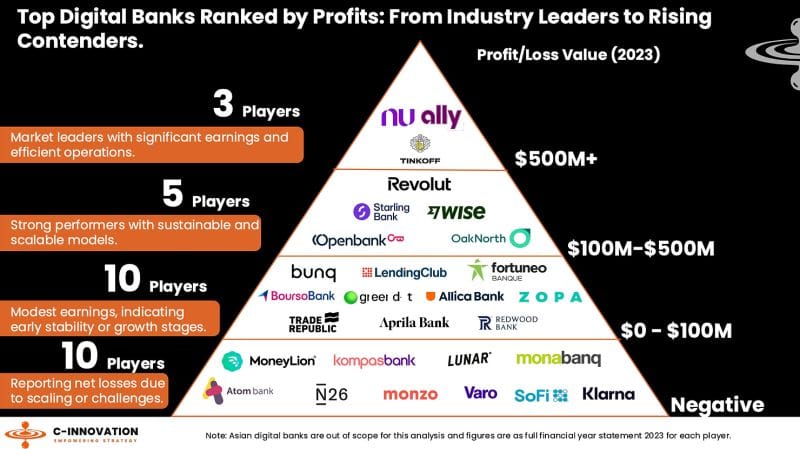

💰 Digital Banking Profitability Review 2024.

DIGITAL BANKING NEWS

🇪🇸 Banco Sabadell offers customers real-time card payment geolocation. The bank is using transaction enrichment technology from Snowdrop Solutions to enable its customers to accurately visualise the locations of their card transactions on a map, along with the merchant name and logo for clearer understanding.

🇸🇪 Qred streamlines credit decisions with open banking tech from Enable Banking. This collaboration enables real-time financial data analysis, helping Qred streamline credit decisions, enhance customer experiences, and expand its offerings to meet the unique needs of entrepreneurs.

🇩🇪 Deutsche Bank shares drop after quarterly profit falls. Net profit attributable to shareholders hit 106 million euros ($110.4 million) in the Q4, compared with the 282.39 million euros forecast in an LSEG poll of analysts. The result marked a significant fall from the 1.461 billion euros achieved in the third quarter.

🇸🇪 UBS and Microsoft unite: co-creating the future of banking with Azure AI. UBS selected Microsoft Azure AI solutions to power “Smart Assistants” that streamline content access and provide real-time information to Client Advisors, boosting efficiency and client engagement.

🇪🇸 BBVA expects to reach 20,000 tech employees in 2025. The profiles most in-demand in the Engineering area continue to be software developers and data engineers, followed by security, infrastructure and architecture specialists. Continue reading

🇩🇰 Danske Bank first in Nordics to adopt BlackRock's Aladdin platform. With this collaboration, the bank aims to increase proactivity and engagement for its investment customers via a more scalable approach to its already existing strong investment competencies.

🇸🇦 Saudi Telecom’s digital bank STC set to launch full operations. It will enable customers to open a bank account and manage their money solely online, or pay their bills, receive salaries and move funds, among others, via non-traditional channels.

🇬🇧 Doo Clearing partnered with Aurum Solution. The integration will enable the broker to comply efficiently with the Financial Conduct Authority’s Client Asset Sourcebook (CASS) regulations. Aurum offers reconciliation software that automates companies’ day-to-day processes.

🇫🇷 Swan adds another $44 million to its Series B. Swan helps other companies offer financial products at scale. The company can generate virtual and physical cards that work with Apple and Google Pay. Cards can be configured by Swan’s corporate clients with spending limits, authorized merchants, and more.

🇬🇧 Sokin secures $15m funding from BlackRock. The funding will enable Sokin to further grow its market share, develop new products which enhance its proposition and significantly scale its team including new offices in London, New York, Toronto and Dubai.

🇬🇧 Lloyds Banking Group appoints Magdalena Lis as Head of Responsible Artificial Intelligence. She will focus on leveraging next-generation technology to enhance Lloyds Banking Group's products and services while implementing necessary safeguards and controls. She brings over 15 years of experience in AI.

🇬🇧 Travel Ledger integrates Revolut. This integration brings Revolut Business accounts, enabling travel businesses to use Revolut’s extensive banking services to automatically settle B2B payments with partners directly through the Travel Ledger platform.

🇦🇺 National Australia Bank scam warnings help Australians abandon suspect payments. NAB pings customers with an alert if a payment appears out of character for them or raises scam concerns. The notices are designed to encourage recipients to stop and check before they send money.

🇨🇭 BIS issues AI guidance for central banks. The guidance covers a wide range of AI use cases in central banking, such as data analysis, research, economic forecasting, payments, supervision, and banknote production. It also identifies key risks such as data security concerns, AI model errors, and reputational challenges.

GOLDEN NUGGET

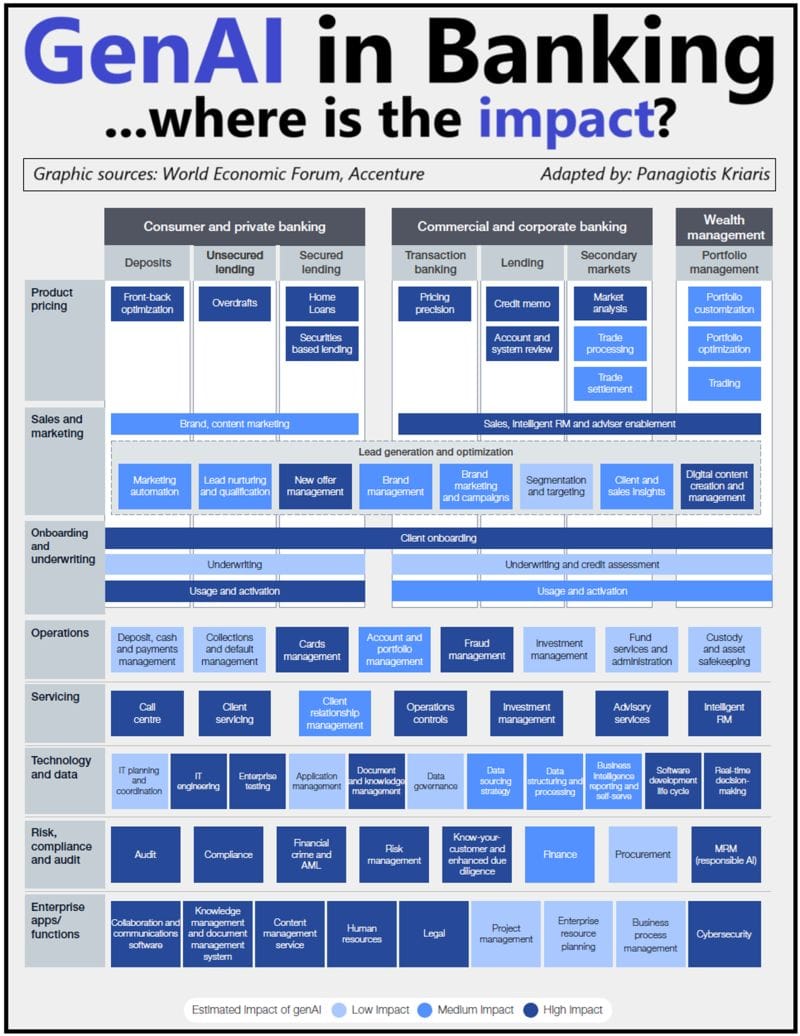

No bank will remain untouched by the #GenAI tsunami. But there is great confusion on the impact and on what to prioritize.

Here are the best practices.

The first step to clear the confusion is to understand what are the main areas of impact and why. Not so much in terms of use cases but of disruption and transformation.

This is my top list:

1. The back-office will be disrupted the most. Most of the processes and repetitive tasks will be completely replaced by GenAI.

2. The front-office will be both replaced and enhanced by #AI. Lower added-value tasks will be replaced to a bigger extent (i.e. chatbots for 1st- level customer support), whereas more customer-facing ones will mostly be enhanced.

3. Hyper-personalization (deliver highly personalized experiences on a massive scale) is one of the biggest opportunities, only because it was so far the bank’s biggest weakness. GenAI will not only allow banks to customize customer interactions but also their outcome: offers, pricing, the whole experience. Marketing will never be the same again.

4. Decisioning will be turbo-charged but not replaced by GenAI: i) the more complex the decision, the higher the degree of enhancement ii) the more at stake, the bigger the need for involving people at the end.

5. Scenario planning and forecasting including financial analysis will be greatly automated by using GenAI data-driven models that can learn from large and diverse data sources. The big change here is the accuracy of the predictions: traditional models were based on historical #data, whereas AI can incorporate dynamic market movements.

6. HR will see a massive transformation. People will not only have to be re-trained and up-skilled but will also see their job descriptions and time allocation adjusted.

Once the big picture is clear, prioritizing the how can be daunting task. The biggest - and most common - mistake is to start with the use cases.

Priority should instead focus on getting 4 areas right using a top-down approach: data, culture, IT and governance:

1. Bring data in an AI-capable format

2. Focus on the people and on the culture

3. Understand how to bridge existing IT infrastructure (many parts of which can be legacy) with GenAI

4. Re-assess your governance model (and make sure it can handle AI challenges, i.e. stemming from regulation)

I highly recommend reading the complete source article by Panagiotis Kriaris for more interesting info on this topic.

Want your message in front of 100.000+ Digital Banking fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.