Crypto’s ‘Debanking’ Battle Heats Up in Washington

Hey Digital Banking Fanatic!

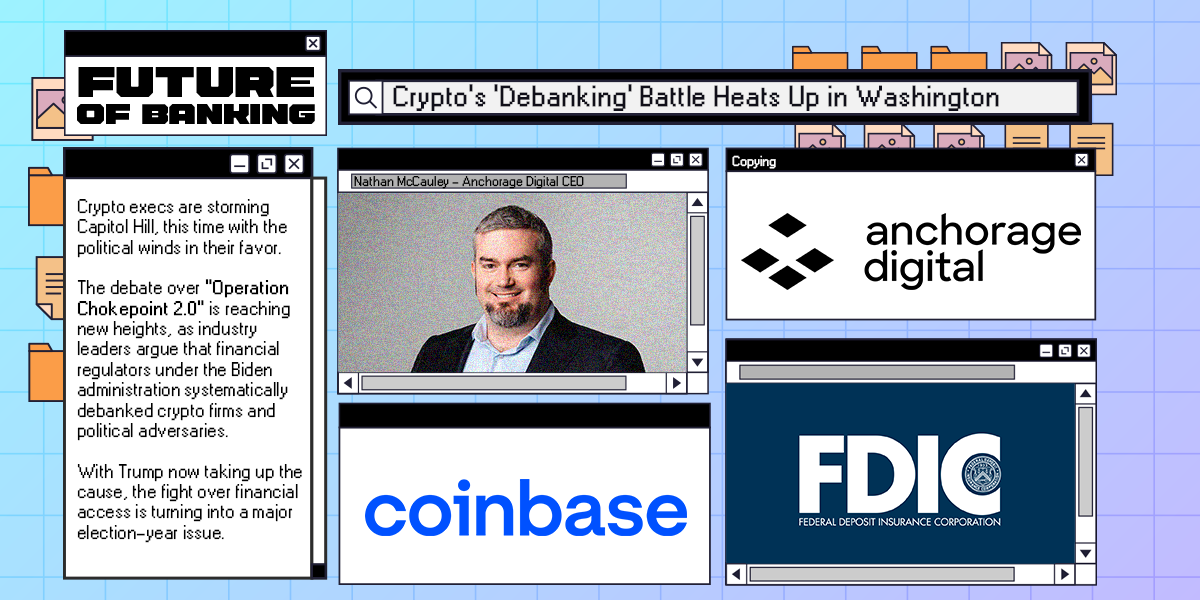

Crypto execs are storming Capitol Hill, this time with the political winds in their favor. The debate over “Operation Chokepoint 2.0” is reaching new heights, as industry leaders argue that financial regulators under the Biden administration systematically debanked crypto firms and political adversaries. With Trump now taking up the cause, the fight over financial access is turning into a major election-year issue.

Anchorage Digital CEO Nathan McCauley testified that his federally chartered crypto bank lost its banking partner without warning, with dozens of others refusing to step in. Meanwhile, Coinbase is calling out the FDIC for allegedly misleading the public about pressure on banks to cut crypto ties. The FDIC, now under a shifting administration, seems to be rethinking its stance, with Acting Chair Travis Hill stating that crypto firms shouldn’t face “time-consuming engagements” just to innovate.

But let’s not forget how we got here—after the FTX collapse and bank failures like Silvergate and Signature, regulators cracked down hard. Now, the pendulum is swinging back, but how long until the next crypto crisis shakes things up again? Stay tuned.

Read more global digital banking updates below 👇 and I'll be back tomorrow!

Cheers,

Stay ahead in FinTech! Subscribe to my Daily FinTech Newsletter for daily updates and breaking news delivered straight to your inbox. Get the essential insights you need and connect with FinTech enthusiasts now!

INSIGHTS

SME-focused neobanks and expense management platforms have transformed financial services across the EU, US, and beyond—fueled by massive investments and skyrocketing valuations.

DIGITAL BANKING NEWS

🇺🇸 Crypto’s ‘Debanking’ debate takes center stage in Washington. Crypto executives recently testified before Congress, arguing that “Operation Chokepoint 2.0” had unfairly targeted crypto companies during the Biden administration by pressuring banks to cut ties with them.

🇦🇷 Ualá announced its conversational AI platform, aimed at transforming customer service powered by OpenAI’s GPT-4 model. According to the company, this technology not only understands user inquiries but also proactively offers personalized solutions, significantly improving the customer experience.

🌏 Standard Chartered launches AI-powered FX insight videos. The bank is using AI to create short videos giving its retail customers in Asia the latest foreign exchange insights. The service will help investors stay abreast of the rapidly changing FX market in an interactive and accessible way.

🇬🇧 UK consumers increasingly moving towards FinTechs and Neobanks for primary bank cards. Digital-only financial providers expanded their overall reach from 16% of adults back in 2018 to a significant 50% in 2024 according to research from RFI Global, the data and insights firm focusing on financial services.

🌎 Banking platform Moneythor lands in Latin America. Regional operations will be led by Enrique Ramos O’Reilly, Moneythor’s President Americas, a 25-year banking and FinTech veteran. The platform helps global financial institutions build deeper, more durable, and valuable relationships with their customers.

🇺🇸 Azura Credit Union modernizes technology infrastructure with Jack Henry. This will empower each local branch to enhance operational efficiencies and gain deeper insights into the unique needs of their communities, enabling the delivery of meaningful solutions.

🇺🇸 Trustly teams up with Spreedly. This collaboration is set to drive improved conversion rates and payment efficiency while expanding the reach of Trustly’s services across US markets. Businesses leveraging Spreedly’s range of payment gateways will gain access to Trustly’s Pay by Bank capabilities.

🇿🇦 FirstRand Group selects Fiserv to accelerate growth and innovation. It will also power its digital transformation and support the broader innovation initiative and growth objectives of its customer franchises FNB (Retail and commercial banking) and RMB (Corporate and investment banking).

🇳🇱 Backbase and Feedzai partner to launch deeply integrated financial crime prevention in the engagement banking platform. The strategic partnership with Feedzai aims to empower banks to tackle the growing challenge of digital fraud while maintaining seamless customer experiences.

🇺🇸 Vantage Bank chooses Finzly to modernize payment operations. The implementation will enable Vantage Bank to meet evolving customer demands while strengthening its core payment capabilities through a fully ISO 20022 native platform.

🇺🇸 P2P launches digital finance platform powered by Mbanq. The P2P app helps users handle their finances in the U.S. and send money to family in Brazil. The financial services provided by the app include U.S. dollar accounts, physical and virtual debit cards, secure money transfers and 24/7 access to financial tools.

GOLDEN NUGGET

What's the difference between an EMI License and a Banking License?

Let’s dive in:

Electronic Money Institutions (EMIs), entities authorized to issue and manage electronic money, operate in a sphere that while similar, is distinct from traditional banks.

E-Money & EMIs Explained:

E-money, essentially digitized cash, is appreciated for its multipurpose convenience, enabling transactions via digital records, prepaid cards, and e-wallets.

EMIs, regulated entities licensed to manage e-money, engage in various financial activities such as:

✔️ Issuance, distribution, and redemption of e-money

✔️ Provision of services that enable transactions with e-money, such as withdrawing cash from a payment account, transferring funds to third parties, and remittance delivery

✔️ Issuance of payment cards that allow withdrawing and depositing cash.

✔️ Providing information about accounts

Key products offered by EMIs include:

☑️ Virtual IBAN accounts (personal and business)

☑️ Merchant accounts

☑️ Physical or virtual payment cards (debit, prepaid, corporate, travel, gift)

☑️ E-wallets

☑️ Cryptocurrency services

☑️ Money transfers and foreign currency exchange services

☑️ BIN sponsorship

There are currently 660+ authorised EMIs in Europe.

Contrastingly, traditional banks, facilitated by banking licenses, offer a broader array of services:

► Manage client deposits

► Offer payment cards

► Offer credit, for example overdrafts, loans, and mortgages

► Deliver payment-related servicing, such as bill payments and money transfers

► Issue other financial products, for example insurance

Stringent regulations, comprehensive compliance, and risk management characterize their operational framework.

Key Differences between EMIs and Banks:

EMIs, often erroneously synonymous with banks, differ primarily in lending capabilities - a service banks provide but EMIs are prohibited from offering.

EMIs can potentially offer operational and technological efficiencies, swifter services, enhanced safety due to non-lending practices, and face fewer regulatory hurdles.

The differences in regulation between banks and EMIs are often due to the fact that banks operate and handle money on a much larger scale than EMIs do.

In Europe, banks typically need a large capital base of at least €5 million, whereas EMIs are smaller businesses and can operate with as little as €350,000.

I highly recommend subscribing for more articles in my newsletter Connecting the dots in FinTech for more interesting info on this topic.

Want your message in front of 100.000+ Digital Banking fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.