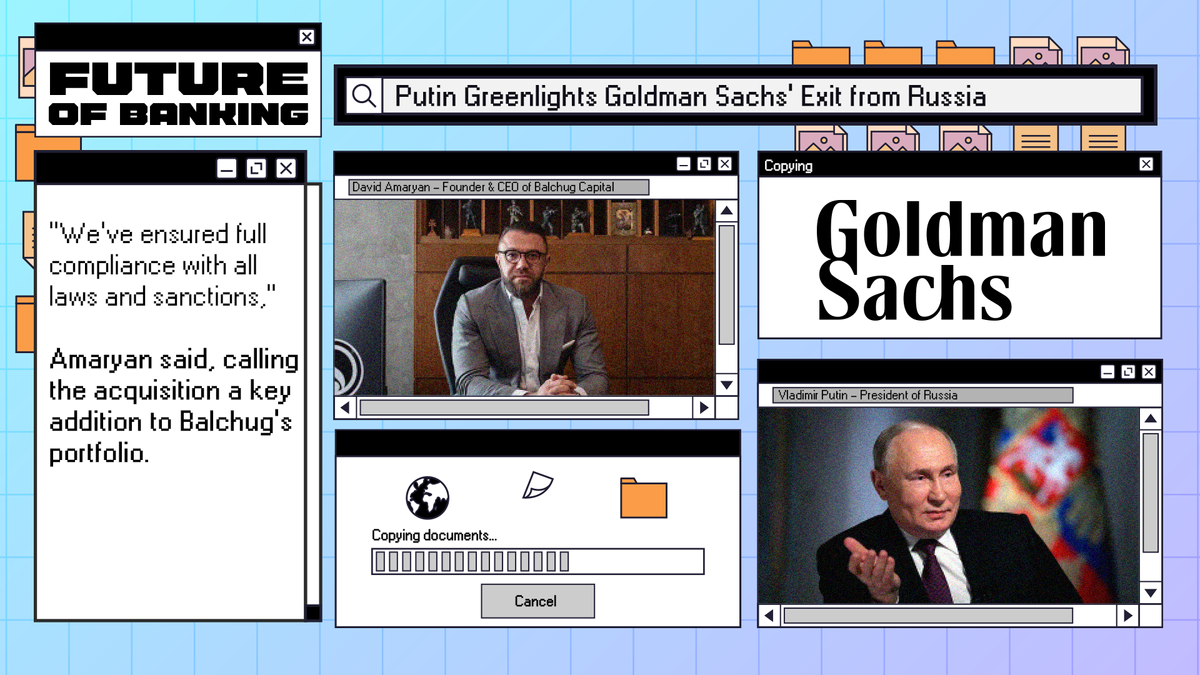

Putin Greenlights Goldman Sachs' Exit from Russia

Hey Banking Fanatic!

Goldman Sachs is officially packing up in Russia! President Vladimir Putin has approved the sale of its Russian division to Balchug Capital, making Goldman one of the few Western banks to fully exit the country.

This follows similar moves—Putin recently allowed Natixis and ING to sell their Russian operations. Meanwhile, Citigroup has wound down most services but still holds $9B in Russian exposure.

Goldman, which first entered Russia in 1998, ranked 230th by assets domestically. The buyer, Armenia-based Balchug Capital, is led by David Amaryan, a former AllianceBernstein and Citigroup exec who’s been snapping up Russian real estate since the war began.

“We’ve ensured full compliance with all laws and sanctions,” Amaryan said, calling the acquisition a key addition to Balchug’s portfolio.

Stay tuned for more Digital Banking updates below 👇. Catch you soon!

Cheers,

P.S. Quick Favor!

I’m helping a friend out with a project, and I thought it might be helpful for some of you. If you’re trying to figure out how to validate your FinTech solution or connect with the right partners, this could be worth a look. It’s all about simple, tailored strategies to help you grow and stay ahead of the game.

👍 Check it out if you're curious!

Discover FinTech innovation across APAC. Stay informed with weekly updates—join now!

INSIGHTS

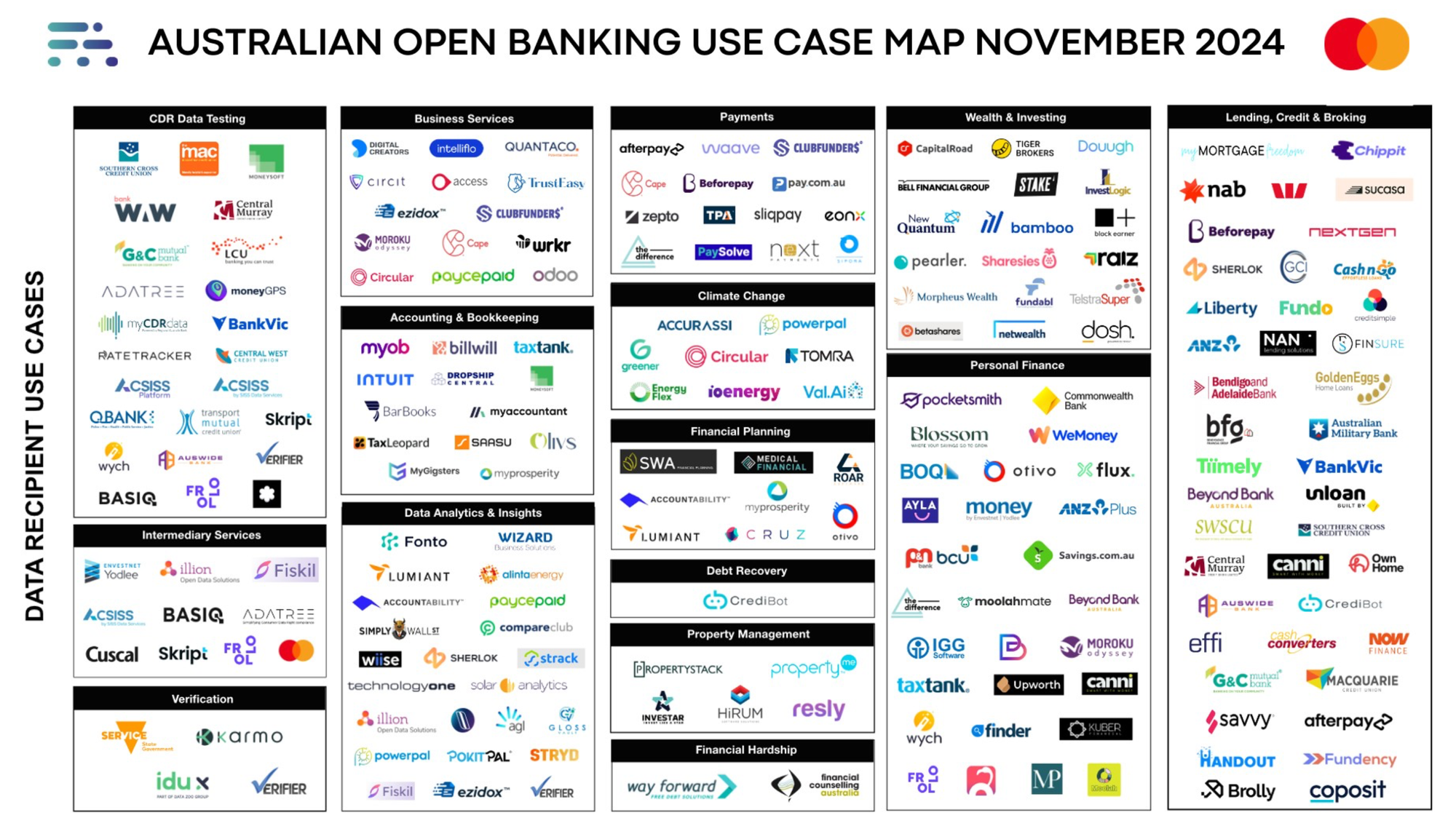

🇦🇺 The Future of Open Banking in Australia

The Australian Open Banking Ecosystem Map and Report👇

DIGITAL BANKING NEWS

🇷🇺 Putin allows Goldman Sachs to sell its business in Russia. This makes the US firm one of the few Western banks to fully exit the country. Goldman has entered into a binding agreement to dispose of its subsidiary, subject to various conditions, according to a person familiar with the matter who asked for anonymity.

🇩🇪 Commerzbank posts 20% hike in annual profit and launches new share buyback. The results come as Commerzbank has been making a case to stand alone, after a surprise stake build from Italy’s lender UniCredit stoked market speculation of interest in a potential takeover.

🇬🇧 Principality Building Society launches OneBanx cash kiosk. The Buckley cash kiosk follows two installations in Principality's Cowbridge and Caerphilly branches. The service represents a significant milestone for the Buckley community, after the high street's final bank closure in 2019.

🇺🇸 IDB Bank has teamed up with ThetaRay, for an AI-powered transaction monitoring solution. The bank will use ThetaRay's cognitive AI technology to enhance its financial crime protections, offering instant risk analysis and transparency in compliance operations.

🇨🇦 TD’s Keeley leaving bank for external role. Vladimir Shpilsky, who was hired by the Toronto-based bank last fall, will join the senior executive team and take on leadership of platforms and technology. Read More

🇬🇧 Taxpayers pay HMRC over £12bn using Pay by Bank. Pay by Bank allows to make secure account to account payments between banks, and is based on open banking APIs and banking infrastructure. Using it means taxpayers do not have to manually enter as much sensitive financial information.

🇦🇺 NAB and Amazon launch PayTo® payment for Amazon.com.au customers. The new PayTo payment option gives Amazon.com.au customers visibility and control over their payments by facilitating the safe authorisation of PayTo arrangements via their online banking platform.

🇺🇸 US Bancorp President Gunjan Kedia to become its first female CEO. She will replace Andy Cecere. "It has been a tremendous honor and a privilege I value deeply, and I believe the time is right to welcome Gunjan warmly to the role I've held for nearly eight years," Cecere said.

GOLDEN NUGGET

𝗪𝗵𝗮𝘁 𝗶𝘀 𝗶𝗻𝘁𝗲𝗿𝗰𝗵𝗮𝗻𝗴𝗲, 𝗮𝗻𝗱 𝘄𝗵𝗮𝘁 𝗳𝗮𝗰𝘁𝗼𝗿𝘀 𝗶𝗺𝗽𝗮𝗰𝘁 𝘁𝗵𝗲 𝗶𝗻𝘁𝗲𝗿𝗰𝗵𝗮𝗻𝗴𝗲 𝗿𝗮𝘁𝗲?

Let’s dive in:

Every time a consumer swipes a card to make a purchase, the merchant pays an interchange fee.

Revenue from the fee gets divided among parties that facilitated the transaction: the banks that send and receive the payment, the card network, the payment processor, and—more recently—FinTechs and businesses that embed payments.

When you take the bird-eye view diagram above as an example:

If a user swipes a card issued by a Neobank, $1.70 (interchange fee) goes to the issuing bank and the card network, $0.50 (acquiring fee) goes to the acquiring bank.

Interchange fees are not always the same though.

𝗪𝗵𝗮𝘁 𝗳𝗮𝗰𝘁𝗼𝗿𝘀 𝗶𝗺𝗽𝗮𝗰𝘁 𝗶𝗻𝘁𝗲𝗿𝗰𝗵𝗮𝗻𝗴𝗲 𝗿𝗮𝘁𝗲?

► Credit vs. Debit

Interchange rates on credit cards are significantly higher than those on debit cards.

► Rewards programs

These benefits are financed through higher interchange rates, and have proven to be very popular with consumers.

► Online vs. Offline

Online purchases are less secure than in-person purchases.

► Consumer vs. Commercial

Cards associated with business or corporate accounts carry higher interchange rates than consumer cards.

► Merchant Category Code (MCC)

Every merchant is categorized by the major card networks according to a Merchant Category Code (MCC). This means that there are different interchange rates depending on whether someone uses a card in a supermarket, a retail store, a gas station, or with some other form of merchant.

► The Card Network

Different card networks charge different rates. Visa and Mastercard are known for charging lower rates. Other networks like AMEX are known for charging higher rates.

► Network partner programs

Visa and Mastercard’s partner programs like VPP (Visa Partner Program) and MPP (Mastercard Partner Program) often give specific retailers interchange rates that are much lower than the networks’ published interchange rates.

► Size of the issuing bank (𝗢𝗡𝗟𝗬 in the US 🇺🇸)

Larger banks are subject to a regulation called the Durbin Amendment that caps interchange rates on consumer debit transactions. Smaller banks are exempt.

As a result, these smaller banks can earn more revenue from interchange rates, which benefits FinTechs and embedded finance businesses that partner with them.

I highly recommend reading more about these topics in Connecting the dots in Pyament for more interesting info on this topic.

Want your message in front of 100.000+ Digital Banking fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn.